2026 Loan Limits Are Here—What First-Time Buyers Need to Know

Key Takeaways

Starting January 1, 2026, you can borrow up to $832,750 on a regular home loan without needing a jumbo mortgage. That's $26,250 more than in 2025. If you live somewhere expensive like San Francisco or New York, your limit jumps to $1,249,125. These higher limits mean more homes are within reach using standard loans with better rates.

What Is the Conforming Loan Limit?

When you buy a home, there's a cap on how much you can borrow with a regular mortgage. This cap is called the "conforming loan limit." If your loan stays under this limit, it's called a conforming loan. Go over the limit, and you need something called a jumbo loan, which usually comes with stricter rules and higher interest rates.

The reason this limit exists comes down to two big names you've probably heard: Fannie Mae and Freddie Mac. These are government-backed companies that buy mortgages from lenders. They can only purchase loans that fall under the conforming limit. When lenders know they can sell your loan to Fannie or Freddie, they're more willing to offer you competitive rates.

Who Decides the Limit?

A government agency called the Federal Housing Finance Agency (FHFA) sets these limits every year. They're required to do this by a law called the Housing and Economic Recovery Act (HERA) from 2008. The FHFA looks at how much home prices went up (or down) over the past year and adjusts the limit to match. For 2026, home prices rose 3.26% on average, so the loan limit went up by the same percentage.

Why Does It Change Every Year?

Home prices don't stay the same from year to year. When prices go up, the old loan limits wouldn't cover as many homes. By law, the FHFA has to update the limits each November based on their House Price Index. This keeps the limits in line with what homes actually cost. One important note: even if home prices drop, the limit won't go down. It just stays flat until prices climb back up.

The New 2026 Limits

Here's what you can borrow starting January 1, 2026:

For most of the country:

• Single-family home: $832,750

• Two-unit property: $1,066,250

• Three-unit property: $1,288,800

• Four-unit property: $1,601,750

For high-cost areas (places like parts of California, New York, or Washington D.C.):

• Single-family home: $1,249,125

• Two-unit property: $1,599,375

• Three-unit property: $1,933,200

• Four-unit property: $2,402,625

Alaska, Hawaii, Guam, and the U.S. Virgin Islands have their own rules. A single-family home there gets the high-cost limit of $1,249,125 as the baseline.

Find Your County's Limit

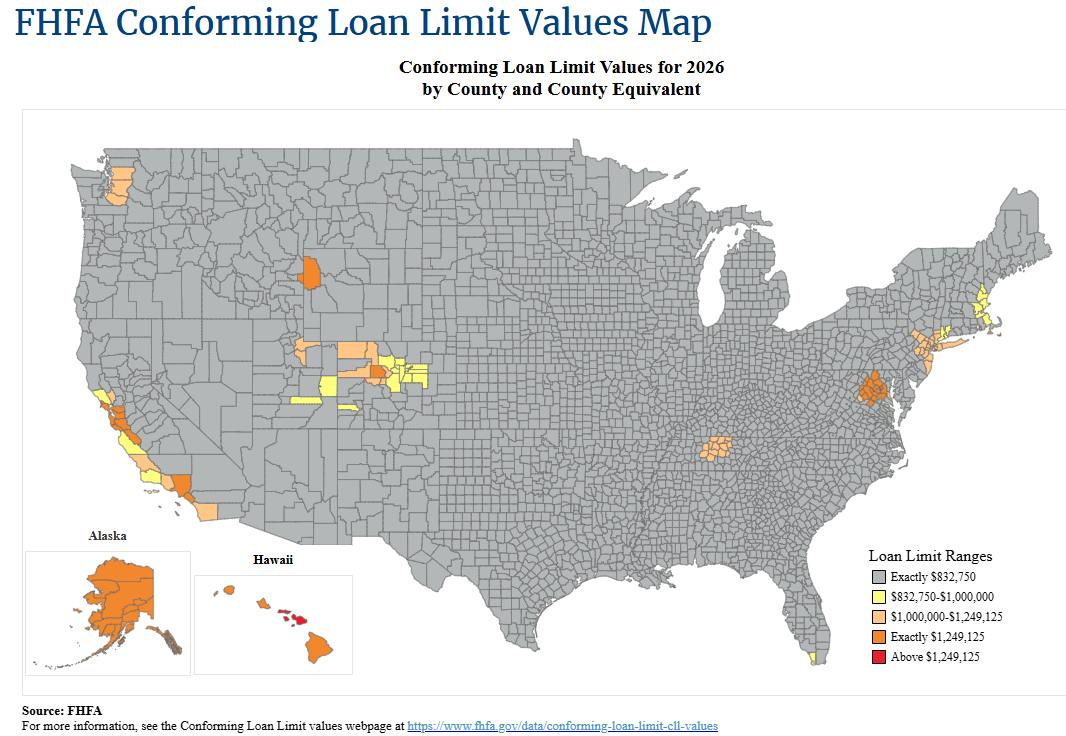

Not sure if you live in a high-cost area? The map shown in this article comes from the FHFA and shows loan limits for every county in the country. The darker shaded areas have higher limits. You can explore the interactive version of this map on the FHFA website. Just hover over or click on your county to see exactly what your local limit is. Many counties fall somewhere between the baseline and the maximum, so it's worth checking your specific area.

What This Means for You as a First-Time Buyer

If you're buying your first home, this is good news. Higher limits mean you can finance a pricier home without getting pushed into jumbo loan territory. Conforming loans typically offer lower interest rates, smaller down payment options, and easier approval requirements. You can check your specific county's limit on the FHFA website since some areas have limits between the baseline and the high-cost ceiling.

Remember, these limits apply to your loan amount, not the home price. If you're putting money down, you can buy a home that costs more than the limit. For example, with a $100,000 down payment, you could buy a home priced at $932,750 and still have a conforming loan.

The mortgage rates displayed on this site are collected daily from publicly available sources provided by more than 600 lenders. Mortgage-Rates.ai does not receive compensation for listing these rates, and all rates are presented as published by the respective lenders. While every effort is made to ensure accuracy, the information may contain errors or omissions. Mortgage rates are highly dependent on an individual’s financial circumstances, credit profile, loan terms, and other factors. As such, the rates you are quoted directly by a lender may differ materially from the rates displayed here.

Users should contact lenders directly to obtain formal, binding loan offers. If you identify any discrepancies in the data or would like to have your institution’s rates included, please contact us at content@mortgage-rates.ai

All logos, trademarks, and brand names appearing on this website are the property of their respective owners.

About the author

mortgage-rates.ai